October 2023 – College Forecast: Skepticism Toward Higher Education Rises

By Matthew Wisehaupt on October 13, 2023

A notable shift in public opinion over the past decade about the value of a college degree may portend a reckoning for the higher education industry in the years ahead — and for the families who are trying to save for and manage the costs. A 2023 survey found disaffection spreading to all age groups, with 56% of Americans saying a four-year college degree isn’t worth the cost due to students graduating with significant debt and a lack of specific job skills vs. 42% who think college is worth it.1 Ten years ago, the survey numbers were almost reversed.

Lower College Enrollment

Public misgivings about college intensified during the pandemic, when academic instruction moved online and families began questioning sky-high tuition costs. This translated into lower enrollment, which continued post-pandemic. For the 2022–2023 school year, the college enrollment rate was 62%, down from 66.2% in 2019–2020. Over the past decade, college enrollment has declined by about 15%.2

There are other factors at play besides public skepticism. A robust job market for less-educated workers has made it easier for high school graduates to justify skipping college and head straight into the labor market. At the same time, alternative forms of job training, such as apprenticeships and certificate programs, have become more prevalent and are increasingly seen as viable educational paths toward landing a good job.

Cost: The Elephant in the Room

A big reason Americans are souring on college is the cost. For the 2022–2023 school year (most recent data available), the average one-year cost for tuition, fees, room, and board was $23,250 for in-state students at a four-year public college, $40,550 for out-of-state students, and $53,430 at a four-year private college.3 But many schools, especially “elite” private colleges, cost substantially more, with some over the $80,000 mark.4

Even with a discount on the sticker price, the total cost over four years is too much for many families to absorb. One result of high sticker prices in recent years has been a surge of interest in public colleges, particularly state flagship universities, many of which offer robust academic and student life opportunities comparable to their private counterparts.

Another factor in the college value proposition is time. Four years (or longer if a student changes majors or doesn’t have enough credits to graduate) is a significant investment of time when compared to a one- or two-year certificate or apprenticeship program. Some students are balking at the traditional time commitment of college and the lost opportunity cost of not entering the job market sooner.5

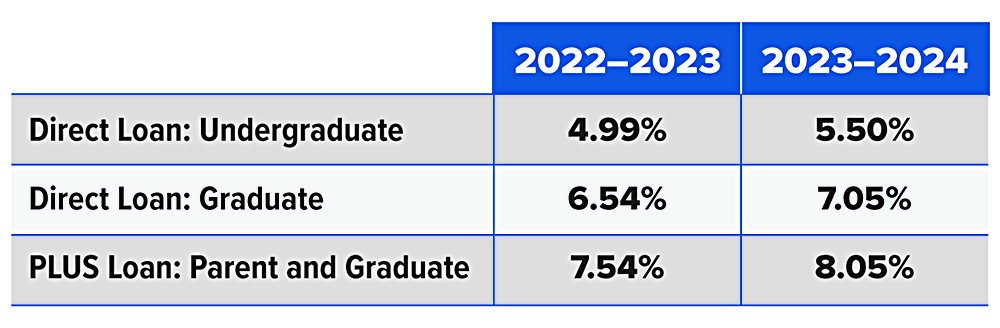

Federal Student Loan Interest Rates

The Burden of Student Loans

Many students need to take out federal, and sometimes private, loans to cover college expenses. Interest rates on federal student loans are based on the rate for the 10-year U.S. Treasury note and reset each year. For the 2023–2024 school year, they have increased again and are now the highest in a decade.

The burden of student loan debt was bubbling in the public consciousness for years but boiled over during the pandemic. Nine payment pauses since March 2020 halted repayment, and widespread calls to cancel student debt led to an executive order in August 2022 cancelling up to $10,000 in federal student loans ($20,000 for Pell Grant recipients) for borrowers with incomes below certain limits, an order that was struck down in June 2023 by the U.S. Supreme Court.6 Also in June, as part of the debt ceiling agreement, Congress ordered an end to the payment pause, and the Department of Education later clarified that payments would start back up in October — a sobering reality for millions of borrowers after three-and-a-half years of payment pauses.7

To help those who may be in financial distress, a new income-driven repayment plan — Saving on a Valuable Education (SAVE) — will allow borrowers to cap their monthly student loan payments at 5% of their discretionary income. It replaces the Revised Pay as You Earn (REPAYE) plan, which capped monthly payments at 10% of discretionary income.8

1) The Wall Street Journal, May 31, 2023 (numbers do not add up to 100% due to rounding)2, 5) The Wall Street Journal, May 29, 20233) The College Board, 20224) Harvard University, 2023; Stanford University, 20236) The New York Times, June 30, 20237) Fiscal Responsibility Act of 2023; U.S. Department of Education, 20238) U.S. Department of Education, 2023